Share Post

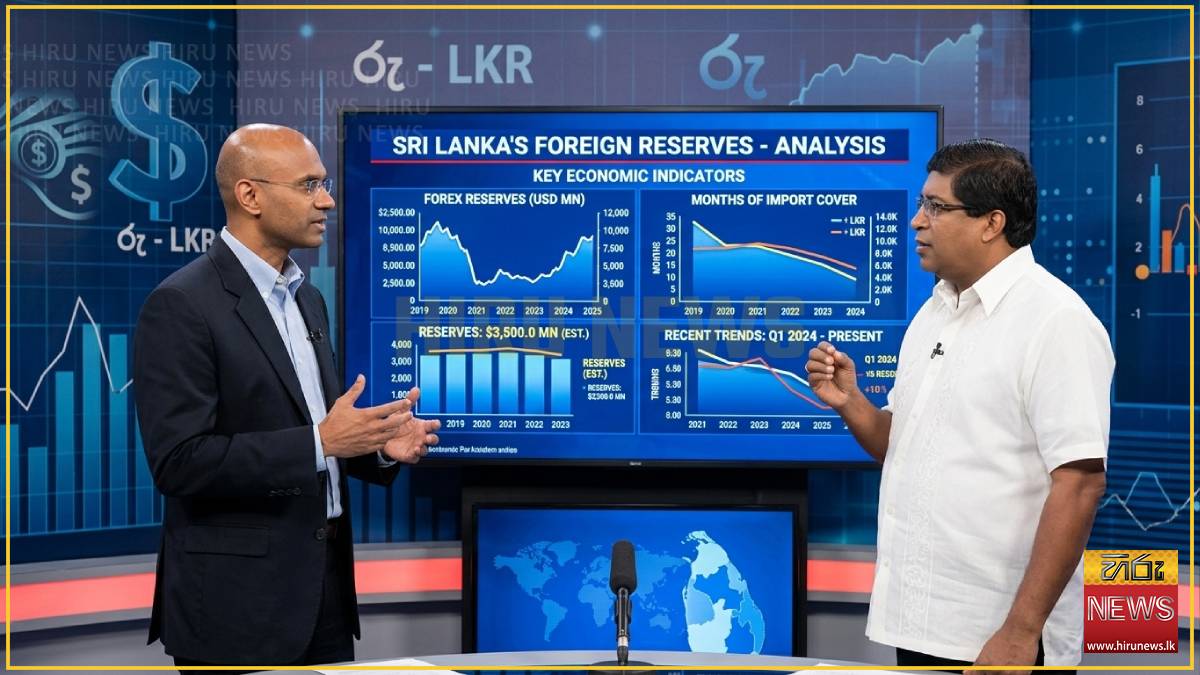

Sri Lanka's official foreign reserves stood at around 6.8 billion US dollars in April, a figure the government and the Central Bank routinely point to as a marker of returning stability. After the worst economic crisis in the country's history, a reserve number climbing back toward seven billion dollars is meant to signal that the worst is behind, that the buffers are being rebuilt, and that the economy is once again standing on solid ground. But two prominent voices are now questioning how much of that headline number is genuinely usable, and how much of it is simply borrowed money dressed up as reserves. Gold FM spoke to economic analyst Ravi Ratnasabapathy and former Finance Minister Ravi Karunanayake, and from two very different vantage points, the two Ravis arrive at a strikingly similar warning.

Former Finance Minister Ravi Karunanayake begins not with the quality of the reserves but with their quantity, and even there, he says, the picture is less reassuring than the official messaging suggests. Before anyone asks whether the reserves are real, he argues, it is worth asking whether there are simply enough of them, because the headline figure is already falling short of the path Sri Lanka committed to under its IMF programme.

"The general reserves of the country should have been, at the end of 25, roughly about 10.2 billion, and at the end of 26, it should be 13.2," he says. "So with that in mind, roughly every month you should be earning 200 million in order to keep the sustainability and the plan of the IMF that is required to be adhered to by the government of Sri Lanka. And today you could see the reserve was 6.8 in March and 6.6 in April. So this is hardly sufficient in order to keep the reserves that are required by the IMF and the government of Sri Lanka.”

In his framing, the country is not just behind on its reserve targets, it is moving in the wrong direction, with April's figure lower than March's, at a moment when the trajectory was supposed to be steadily upward.

But economic analyst Ravi Ratnasabapathy says the problem runs deeper than the number simply being too small. The more serious issue, he argues, is what the number is actually made of. When you break the reserve figure open and look at its components, he says, more than half of it turns out to be money that Sri Lanka does not really own.

"As per February 2026, gross official reserves is 7.27 billion dollars," he explains. "But this includes international swaps of 1,923 million dollars, and domestic forex swaps of 2,030 million. So if you subtract, you've got about 3,923 million. Something more than half of your gross reserves is actually money that you have temporarily borrowed from overseas or from the local bank sector, and it is showing as reserves. They don't really reflect the temporary nature. So it may be giving a somewhat misleading signal to the market about the strength of what you have, because you had to return it at the end of the period.” His point is that a reserve figure is supposed to communicate strength, the capacity to absorb a shock or defend the currency, but a figure padded with borrowed swaps communicates a strength that is not fully there. The money is on the books today, but it is owed back tomorrow.

Karunanayake's own breakdown of the reserves arrives at much the same conclusion, from the perspective of someone who has sat in the Finance Minister's chair. He says the reserve build-up has come from three identifiable sources, and that none of them represent the organic, lasting growth the country actually needs. "The build-up of the reserves comes from three different areas," he says. "One is the swaps that are there, the 1.5 and the Indian swap, that comes up to about 2 billion in swaps. Then you have the IMF loans that are there, which amount to about another 1.2. Then you could see that the creation of reserves was unusual at the end of December 25. There were temporary commercial swaps that were taken in. Now, swaps would mean the Central Bank issues the currency, buys it from the domestic banks on a swap, that is short-term. These are short-term, they are not geared at long-term organic growth. They are looked at just to meet the expectation, far from the reserve that is required. There has to be long-term reserve generation, which is organic in nature."

Swaps, IMF loans, and unusual end-of-year commercial arrangements: in Karunanayake's accounting, the reserve number is less a record of what the country has earned than a record of what it has arranged.

So if the reserves are largely borrowed, the question becomes how they came to be built that way in the first place. Ratnasabapathy traces the pattern back to a deliberate decision by the Central Bank, and warns that it is the same mechanism that has repeatedly landed Sri Lanka in trouble. The reserves, he says, have been accumulated not through earnings but through the creation of new money to buy and swap foreign exchange, a process that has been running since 2024.

"The Central Bank has actually been printing money from 2024 onwards," he says. "First through what they call open market operations during the second half of 2024, and then in 2025, buying and swapping foreign exchange with the local commercial banks, which is part of what appears as reserves. So whenever the Central Bank buys or borrows foreign exchange from the market, they offer in return money that they create newly. The problem with this is that this new money starts getting lent out into the market by the commercial banks, and that drives imports. So this was actually a fundamental imbalance that was brewing for some time, which the crisis in the Middle East seems to have precipitated." In his telling, the reserve build-up and the import pressure are two faces of the same coin. The newly created rupees that bought the dollars did not vanish once the dollars were on the books, they flowed into the banking system, became credit, and came back out as demand for imports.

So what is the way out? Ratnasabapathy is clear that the answer does not lie in import controls or selective restrictions, but in monetary policy, and specifically in the level of interest rates. The fundamental problem, as he sees it, is that borrowing has simply become too cheap, and cheap debt is fuelling a pace of credit growth the economy cannot safely sustain. "The interest rates are too low," he says. "You can see credit is expanding very fast. The record was in November last year, and now in March again credit expanded sharply. Credit is growing too fast, and that's because debt is cheap. So the rates do need to move up to tighten that. It's too loose, in my view." For Ratnasabapathy, until rates rise enough to slow that credit expansion, every attempt to build reserves risks simply feeding the next wave of imports, and the cycle continues.

With reserves largely borrowed, credit running hot, and interest rates that he considers too low, the message from the two Ravis converges on a single point. On paper, Sri Lanka holds close to seven billion dollars in reserves. In practice, both the former Finance Minister and the economic analyst say a large share of that is borrowed through swaps and loans that must eventually be returned, and that the figure is running behind the trajectory the IMF programme requires. Their shared warning is simple. Until Sri Lanka builds reserves organically, through exports and real earnings rather than newly created money, the headline number will remain more reassuring than it deserves to be.

Former Finance Minister Ravi Karunanayake begins not with the quality of the reserves but with their quantity, and even there, he says, the picture is less reassuring than the official messaging suggests. Before anyone asks whether the reserves are real, he argues, it is worth asking whether there are simply enough of them, because the headline figure is already falling short of the path Sri Lanka committed to under its IMF programme.

"The general reserves of the country should have been, at the end of 25, roughly about 10.2 billion, and at the end of 26, it should be 13.2," he says. "So with that in mind, roughly every month you should be earning 200 million in order to keep the sustainability and the plan of the IMF that is required to be adhered to by the government of Sri Lanka. And today you could see the reserve was 6.8 in March and 6.6 in April. So this is hardly sufficient in order to keep the reserves that are required by the IMF and the government of Sri Lanka.”

In his framing, the country is not just behind on its reserve targets, it is moving in the wrong direction, with April's figure lower than March's, at a moment when the trajectory was supposed to be steadily upward.

But economic analyst Ravi Ratnasabapathy says the problem runs deeper than the number simply being too small. The more serious issue, he argues, is what the number is actually made of. When you break the reserve figure open and look at its components, he says, more than half of it turns out to be money that Sri Lanka does not really own.

"As per February 2026, gross official reserves is 7.27 billion dollars," he explains. "But this includes international swaps of 1,923 million dollars, and domestic forex swaps of 2,030 million. So if you subtract, you've got about 3,923 million. Something more than half of your gross reserves is actually money that you have temporarily borrowed from overseas or from the local bank sector, and it is showing as reserves. They don't really reflect the temporary nature. So it may be giving a somewhat misleading signal to the market about the strength of what you have, because you had to return it at the end of the period.” His point is that a reserve figure is supposed to communicate strength, the capacity to absorb a shock or defend the currency, but a figure padded with borrowed swaps communicates a strength that is not fully there. The money is on the books today, but it is owed back tomorrow.

Karunanayake's own breakdown of the reserves arrives at much the same conclusion, from the perspective of someone who has sat in the Finance Minister's chair. He says the reserve build-up has come from three identifiable sources, and that none of them represent the organic, lasting growth the country actually needs. "The build-up of the reserves comes from three different areas," he says. "One is the swaps that are there, the 1.5 and the Indian swap, that comes up to about 2 billion in swaps. Then you have the IMF loans that are there, which amount to about another 1.2. Then you could see that the creation of reserves was unusual at the end of December 25. There were temporary commercial swaps that were taken in. Now, swaps would mean the Central Bank issues the currency, buys it from the domestic banks on a swap, that is short-term. These are short-term, they are not geared at long-term organic growth. They are looked at just to meet the expectation, far from the reserve that is required. There has to be long-term reserve generation, which is organic in nature."

Swaps, IMF loans, and unusual end-of-year commercial arrangements: in Karunanayake's accounting, the reserve number is less a record of what the country has earned than a record of what it has arranged.

So if the reserves are largely borrowed, the question becomes how they came to be built that way in the first place. Ratnasabapathy traces the pattern back to a deliberate decision by the Central Bank, and warns that it is the same mechanism that has repeatedly landed Sri Lanka in trouble. The reserves, he says, have been accumulated not through earnings but through the creation of new money to buy and swap foreign exchange, a process that has been running since 2024.

"The Central Bank has actually been printing money from 2024 onwards," he says. "First through what they call open market operations during the second half of 2024, and then in 2025, buying and swapping foreign exchange with the local commercial banks, which is part of what appears as reserves. So whenever the Central Bank buys or borrows foreign exchange from the market, they offer in return money that they create newly. The problem with this is that this new money starts getting lent out into the market by the commercial banks, and that drives imports. So this was actually a fundamental imbalance that was brewing for some time, which the crisis in the Middle East seems to have precipitated." In his telling, the reserve build-up and the import pressure are two faces of the same coin. The newly created rupees that bought the dollars did not vanish once the dollars were on the books, they flowed into the banking system, became credit, and came back out as demand for imports.

So what is the way out? Ratnasabapathy is clear that the answer does not lie in import controls or selective restrictions, but in monetary policy, and specifically in the level of interest rates. The fundamental problem, as he sees it, is that borrowing has simply become too cheap, and cheap debt is fuelling a pace of credit growth the economy cannot safely sustain. "The interest rates are too low," he says. "You can see credit is expanding very fast. The record was in November last year, and now in March again credit expanded sharply. Credit is growing too fast, and that's because debt is cheap. So the rates do need to move up to tighten that. It's too loose, in my view." For Ratnasabapathy, until rates rise enough to slow that credit expansion, every attempt to build reserves risks simply feeding the next wave of imports, and the cycle continues.

With reserves largely borrowed, credit running hot, and interest rates that he considers too low, the message from the two Ravis converges on a single point. On paper, Sri Lanka holds close to seven billion dollars in reserves. In practice, both the former Finance Minister and the economic analyst say a large share of that is borrowed through swaps and loans that must eventually be returned, and that the figure is running behind the trajectory the IMF programme requires. Their shared warning is simple. Until Sri Lanka builds reserves organically, through exports and real earnings rather than newly created money, the headline number will remain more reassuring than it deserves to be.

Latest News

Sampath Bank brings Google Pay to Sri Lankan card users

Local

07 July 2026

Monaco bombing suspect found dead in Kyiv

Local

07 July 2026

Chinese official sentenced to death in record bribery case

Local

07 July 2026

Fuel limitations no more for ministers and public officials

Local

07 July 2026

Blasts rock Damascus during Macron visit

Local

07 July 2026

Court orders postmortem for 27 victims of Negombo Prison clash

Local

07 July 2026

Free Lawyers condemn shooting of inmates at Negombo prison

Local

07 July 2026

Krrish deal case called for November 16

Local

07 July 2026

6 suspects linked to narcotics trade arrested

Local

07 July 2026

Environment Ministry yet to establish mechanism to collect polythene bag levies

Local

07 July 2026